You are here

The Next Fiscal Cliff: Big Tax Decisions to Make in 2025

In 2017, Congress and the President enacted the Tax Cuts and Jobs Act (TCJA), which made significant changes to the tax code for individuals and corporations. Most of the changes to the corporate tax code were legislated to be permanent law, but many of the individual income tax provisions, as well as certain other provisions, are slated to expire at the end of December 2025. That deadline sets up a significant decision point for policymakers, with major implications for the country’s fiscal outlook.

Trillions of dollars are at stake. When the TCJA was enacted, the Congressional Budget Office (CBO) and the Joint Committee on Taxation (JCT) estimated that it would increase federal deficits by $1.4 trillion over a 10-year period, almost exclusively by reducing revenues.

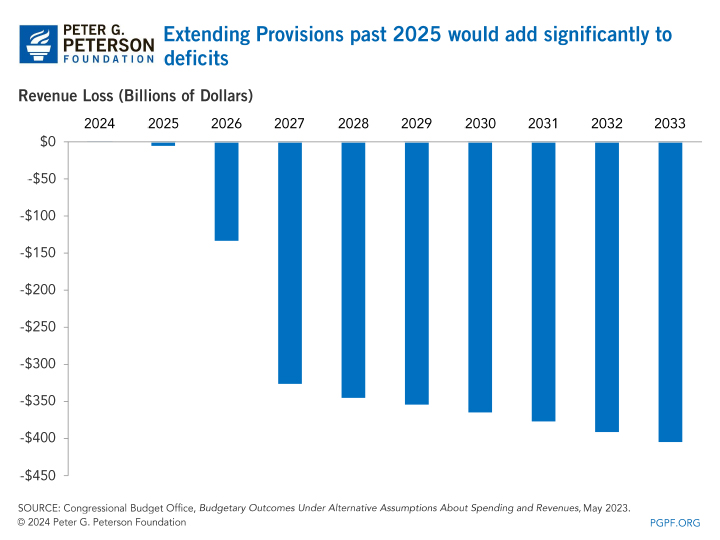

Extending all provisions from the TCJA that are set to expire at the end of 2025 would increase deficits by $2.7 trillion from 2024 to 2033, according to CBO and JCT. The largest categories of expirations — nearly all from provisions related to individual income taxes — are included below, along with their effect on the deficit.

Extending TCJA provisions set to expire in 2025 would increase future deficits

Impact on Deficit (Billions of Dollars)

| Provision | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2024-2033 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Individual and Families | $0 | $0 | -$122 | -$225 | -$233 | -$239 | -$247 | -$255 | -$264 | -$272 | -$1,856 |

| Alternative Minimum Tax | $0 | $0 | -$40 | -$134 | -$135 | -$142 | -$148 | -$156 | -$163 | -$171 | -$1,088 |

| Itemized Deductions | $0 | $0 | $67 | $108 | $105 | $112 | $119 | $125 | $132 | $139 | $908 |

| “Pass-Through” Deduction | $0 | -$6 | -$37 | -$63 | -$68 | -$70 | -$72 | -$75 | -$77 | -$80 | -$548 |

| Estate & Gift Tax Exemptions | $0 | $1 | -$3 | -$14 | -$16 | -$16 | -$17 | -$19 | -$20 | -$21 | -$126 |

| Total | $0 | -$6 | -$134 | -$327 | -$346 | -$355 | -$366 | -$378 | -$392 | -$406 | -$2,705 |

SOURCE: Congressional Budget Office Budgetary Outcomes Under Alternative Assumptions About Spending and Revenues, May 2023.

NOTES: The TCJA’s Individual Income Tax Provisions includes Individual and Families, Alternative Minimum Tax, Itemized Deductions and the “Pass-Through” deduction.

© 2024 Peter G. Peterson Foundation

Extending the TCJA’s Individual Income Tax Provisions

Changes to marginal tax rates and brackets, itemized deductions, tax exemptions, credits, and other portions of the federal tax system are set to expire at the end of December 2025. If extended, those individual income tax provisions would increase federal deficits by $2.6 trillion through 2033, according to CBO and JCT. Below is a brief summary of significant provisions and the estimated budgetary effects prepared by CBO and JCT.

Individuals and Families (–$1.9 Trillion)

The estimates below reflect the effect of the largest provisions expiring at the end of December 2025; the individual estimates may not include potential interaction effects of permanently extending the provisions together.

- Changes to tax brackets and rates: −$1.8 trillion. The TCJA lowered most individual income tax rates and altered most income tax thresholds. While maintaining the 7-bracket structure, the combination of lowering most of the tax rates and raising some of the thresholds, particularly for joint filers, significantly reduced the amount of individual income taxes collected. Extending those provisions would keep rates and brackets at their lower or altered levels, thereby reducing revenues by $1.8 trillion through 2033 relative to letting the changes expire.

- Increasing the standard deduction: −$1.0 trillion. The TCJA also nearly doubled the standard deduction, the specific dollar amount that reduces the amount of income a taxpayer who does not itemize is taxed on (which was 92 percent of all taxpayers in 2021). Extending this provision would reduce revenues by an estimated $1.0 trillion through 2033.

- Expansion of the child tax credit: −$0.6 trillion. The TCJA expanded the child tax credit (CTC), which applies to qualifying dependents under the age of 17, doubling the maximum credit from $1,000 to $2,000 per child. It also increased the phase-out threshold from $75,000 for single and $110,000 for joint filers to $200,000 and $400,000, respectively. Extending this provision would reduce revenues by an estimated $604 billion over the following several years.

- Suspension of the personal exemption: $1.6 trillion. The TCJA eliminated personal exemptions (a dollar amount that can be deducted from an individual's total income). Extending the suspension of the personal exemption in isolation would generate an estimated $1.6 trillion in revenues through 2033.

The TCJA changed income tax brackets, significantly reducing revenues

| Previous Law | Tax Cuts and Jobs Act | ||||

|---|---|---|---|---|---|

| Taxable Income ($) | Tax Rate (%) | Taxable Income ($) | Tax Rate (%) | ||

| Single Filers (Joint Filers) | Single Filers (Joint Filers) | ||||

| Over | But not over | Over | But not over | ||

| 0 (0) | $9,925(19,050) | 10 | 0 (0) | 9,525 (19,050) | 10 |

| 9,525 (19,050) | 38,700 (77,400) | 15 | 9,525 (19,050) | 38,700 (77,400) | 12 |

| 38,700 (77,400) | 93,700 (156,150) | 25 | 38,700 (77,400) | 82,500 (165,000) | 22 |

| 93,700 (156,150) | 195,450 (237,950) | 28 | 82,500 (165,000) | 157,500 (315,000) | 24 |

| 195,450 (237,950) | 424,950 (424,950) | 33 | 157,500 (315,000) | 200,000 (400,000) | 32 |

| 424,950 (424,950) | 426,700 (480,050) | 35 | 200,000 (400,000) | 500,000 (600,000) | 35 |

| 426,700 (480,050) | and over | 39.6 | 500,000 (600,000) | and over | 37 |

Tax Policy Center, How did the Tax Cuts and Jobs Act change personal taxes? , 2022.

NOTES: Income levels are for 2018

© 2024 Peter G. Peterson Foundation

Alternative Minimum Tax (−$1.1 trillion)

The alternative minimum tax (AMT), which applies to individual income taxes, was created to address concerns that high-income persons were avoiding paying income tax by setting limits on certain tax benefits, ensuring taxpayers have to pay at least a minimum amount of tax. The TCJA raised the AMT exemption amount, meaning the amount of income free from being taxed, and increased the phase-out income threshold (the gradual tax reduction as the taxpayer’s income approaches the upper limit). In 2017, before the TCJA, about 3 percent of households paid the AMT. By 2019, just 0.1 percent of households paid the AMT. Extending the raised AMT exemption level would keep the number of households subject to the AMT, most of which are high-income, comparatively low, and reduce revenues by $1.1 trillion through 2033.

Itemized Deductions ($0.9 trillion)

The TCJA made several changes to itemized deductions, which allow individuals to subtract certain expenses from their taxable income.

The TCJA changed several itemized deductions

| Provision | Description |

|---|---|

| Public Charity Cash Contributions | Increased the percentage limitation on cash contributions to public charities from 50 percent to 60 percent to incentivize charitable giving |

| Qualified Residence Loan | Reduced the amount of interest a taxpayer can deduct on a qualified residence loan from $500,000 for single and $1 million for joint filers to $375,000 and $750,000, respectively |

| State and Local Tax (SALT) | Capped SALT, a deduction permitting taxpayers who itemize to deduct certain taxes paid to state and local governments, at $10,000 per year (it was not capped previously) |

| Personal Casualty Standards | Generally eliminated qualification unless the loss was incurred from a federally declared disaster |

| Suspension of limitations on itemized deductions | Before TCJA, taxpayers had to abide by the Pease limitation, a provision reducing the value of itemized deductions for high-income individuals. In 2018, the Pease limitation was suspended |

| Miscellaneous itemized deductions | Before TCJA, taxpayers had to abide by the Pease limitation, a provision reducing the value of itemized deductions for high-income individuals. In 2018, the Pease limitation was suspended |

SOURCE: Tax Policy Center, How did the TCJA change the standard deduction and itemized deductions?, 2022.

NOTES: Income levels are for 2018.

© 2024 Peter G. Peterson Foundation

The most significant change to itemized deductions was capping the state and local tax deduction (SALT) at $10,000. Before the TCJA, when SALT was uncapped, about 30 percent of taxpayers claimed the deduction, with high-income households more likely to benefit. After the TCJA, the amount of taxpayers claiming the now-capped deduction fell by nearly two-thirds, although the benefits were still disproportionately accrued by households with incomes over $200,000. The Tax Foundation estimates that eliminating the SALT deduction altogether would generate an additional $2 trillion in revenues through 2033.

Pass-Through Deduction (–$0.5 trillion)

The TCJA also created a new “pass-through” deduction for households with income earned from partnerships, sole proprietorships, and S corporations. That deduction allows individuals to deduct business losses against income from other sources, as opposed to corporation losses that must offset income earned within the corporation. Up to 20 percent of income from such sources can be deducted from fillers' individual income taxes, although the deduction varies depending on factors such as the type of business and total income of its owner. Extending this provision reduces revenues by an estimated $548 billion.

Doubling the Exemption for the Estate Tax (–$0.1 trillion)

In addition to tax provisions affecting individual income taxes, another major change in the TCJA affected estate taxation.

The TCJA doubled the estate tax (a tax on property transferred from deceased persons to heirs) exemption to $22.4 million for those filing jointly and $11.2 for single filers (in 2017 dollars) while continuing to index exemption levels for inflation. The TCJA kept the estate tax rate at 40 percent. Extending this provision would reduce revenues by an estimated $126 billion over the following decade.

How Would Extending Certain TCJA Provisions Impact Deficits and the Debt?

At the end of 2023, debt held by the public represented 97 percent of GDP. Under current law, under which certain provisions of the TCJA would expire, CBO currently projects that such debt will exceed its post-World War II high of 106 percent in 2028 and represent 114 percent in 2033. The Committee for Responsible Federal Budget estimates that extending the TCJA would increase debt held by the public by an additional 10 percentage points to 124 percent of GDP in 2033.

Conclusion

The TCJA included a wide range of provisions, many of which could be defensible or worthy of consideration as part of an overall tax regime. However, taken as a whole, it is undeniable that the TCJA made the country’s fiscal outlook worse, and extending its deficit-increasing provisions makes the debt trajectory even more daunting. As 2025 approaches, policymakers must consider the benefits of the TCJA against the impact of possible extensions on the growing debt.

Related: How Would the Tax Relief for American Families and Workers Act Change Federal Tax Law?

Image credit: Photo by Chip Somodevilla/Getty Images