You are here

Trustees Warn: Social Security’s Total Costs Next Year to Exceed Income for First Time Since 1982

Last week, the Social Security Trustees released a report on the health of the Social Security program’s finances. The report anticipates that in 2020 — for the first time since 1982 — the program’s total costs will exceed its total income. Without policy changes, costs are expected to exceed income every year thereafter; such a trend threatens the future of the program, which is critical to the financial security of millions of Americans.

Social Security provides financial assistance through two components — Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI). OASI provides benefits for retired workers and their families, as well as survivors of deceased workers; DI provides benefits for disabled workers and their families.

Each component has its own trust fund, which is an accounting mechanism used to track the receipts credited to the program and the benefits that have been paid. Excess revenues generated in the past were not invested in outside assets, but were spent on other programs during those years; the trust fund was credited with special Treasury securities to record the surpluses. Today, with Social Security running a deficit, those securities must be redeemed and the federal government must borrow to cover the program’s expenditures.

In their report, the Trustees find that:

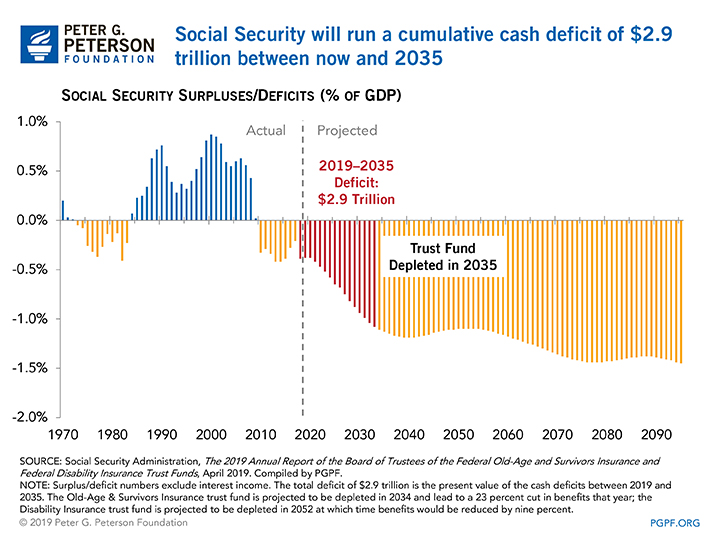

- The OASI trust fund will be depleted in 2034 — the same as reported last year. At that point, beneficiaries would be subject to an immediate 23 percent reduction in benefits.

- The outlook for the DI trust fund has gotten markedly better. It is estimated to be depleted in 2052 — 20 years later than projected last year. Upon depletion, beneficiaries would be subject to a cut in benefits of 9 percent.

- The lengthened period of solvency for the DI trust fund is the result of declining disability applications in recent years as well a revision in the projected rate of disability among the population.

The Trustees emphasize the value of addressing reforms quickly:

“The Trustees recommend that lawmakers address the projected trust fund shortfalls in a timely way in order to phase in necessary changes gradually and give workers and beneficiaries time to adjust to them ... With informed discussion, creative thinking, and timely legislative action, Social Security can continue to protect future generations.”

Key drivers of insolvency

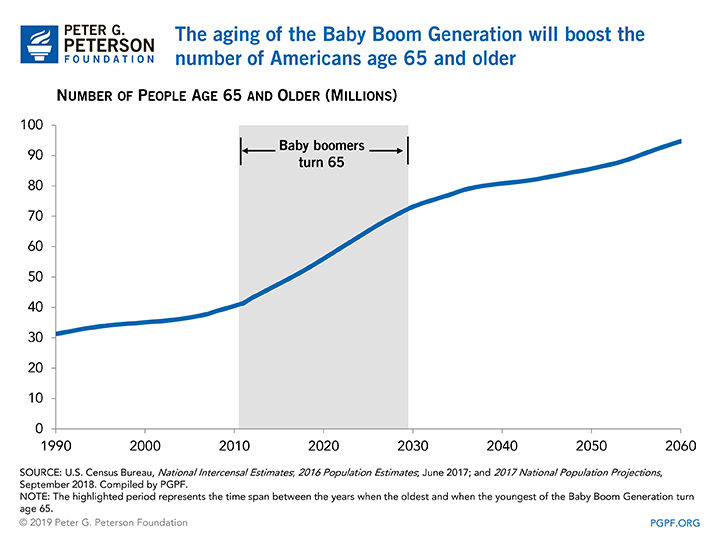

The aging of the population creates serious financial challenges for OASI. As baby boomers retire and life expectancy continues to increase, the number of Social Security beneficiaries is projected to climb sharply. By 2035, the total number of beneficiaries in the OASI program is projected to reach 73 million — about 35 percent more than in 2018.

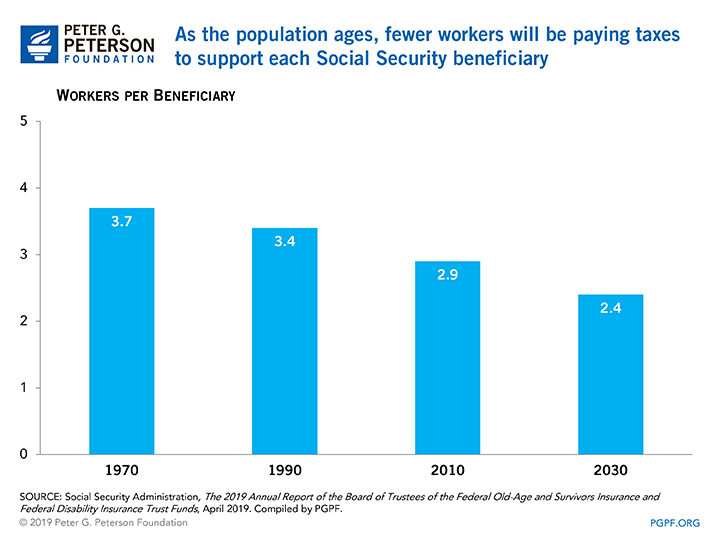

Over the same period, the ratio of workers paying taxes to support each Social Security beneficiary will decline significantly from 3:1 to 2:1. In 1970, that ratio was nearly 4:1. The financial impact of the changes in these ratios is very significant.

The predictable, growing mismatch between the number of people paying into Social Security and the number receiving benefits will cause spending on the program to increase significantly faster than the amount of revenues collected to cover it. As a result, deficits will persist and grow.

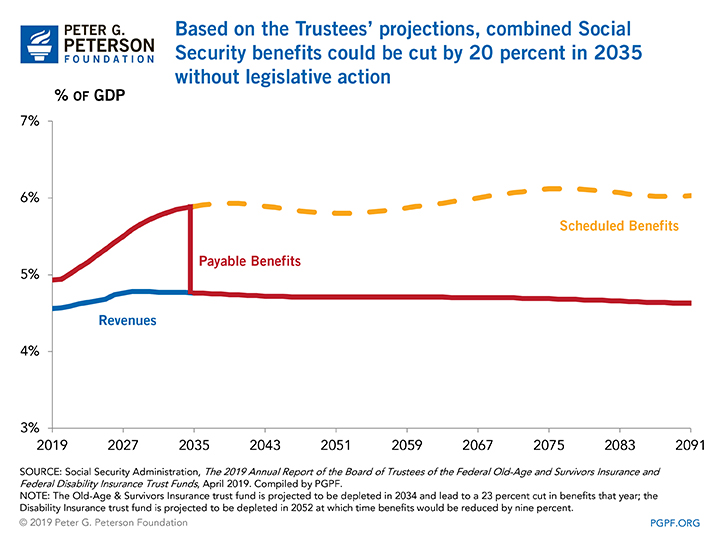

Absent legislative action, once the OASI trust fund is exhausted in 2034, Social Security will no longer be able to pay full benefits, and retirees could face an immediate 23 percent cut in their scheduled benefits. The DI trust fund is expected to be exhausted in 2052, at which point it will be able to pay 91 percent of its obligations (a nine percent cut in benefits).

The exhaustion date of the DI trust fund has been extended significantly in this report — from 2032 to 2052. New applications for the program have continued to decline, and the number of beneficiaries has also been dropping. As a result, the Trustees have adjusted their underlying assumptions about the incidence of disability, which further lengthened the projected exhaustion date of the trust fund.

By contrast, the Congressional Budget Office (CBO) has a less optimistic projection which estimates that the Disability Insurance trust fund would be depleted in 2027. This difference stems largely from CBO’s projections of a larger number of beneficiaries than the amount that was estimated by the Social Security Trustees.

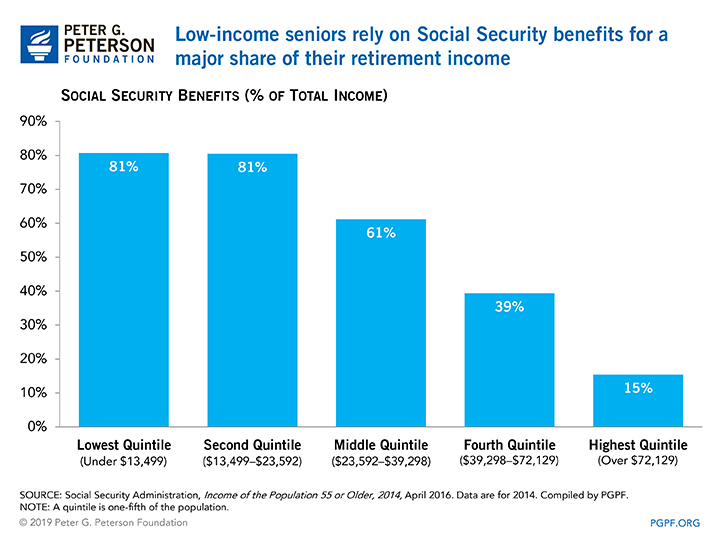

A reduction in benefits of 20 percent or more would impose significant burdens on all recipients, but especially low-income seniors because Social Security is a primary source of their income. Social Security provides more than 80 percent of the income of seniors in the bottom 40 percent of the income distribution (those with $23,592 or less in total income).

Trust Funds

The Social Security trust funds are used to conduct the financial operations of the OASI and DI programs. Income from taxes and other sources are credited to the funds, and disbursements for benefits and administrative costs are debited from their balances. Although many believe that the existence of trust funds guarantees the sustainability of programs in the future, they are simply accounting mechanisms that are part of the way the federal government keeps its books.

The actual cash inflows and outflows of Social Security and other programs with trust funds are combined with the rest of the federal budget, and therefore surpluses in such programs have served to reduce the amount that the government has had to borrow for other programs. Trust funds do not hold their own outside investment assets; they are credited with special Treasury securities that effectively serve as IOUs from one part of the government to another.

Even though the Social Security trust funds are expected to have positive “balances” into the 2030s, beginning in 2010, the Treasury has had to borrow funds from the public to cover deficits in the program. Ultimately, trust fund income and outlays are not separate from the rest of the federal budget, and therefore the sustainability of trust fund programs, like Social Security, depends on the overall sustainability of the federal government.

Solutions

Long-term demographic trends are clear and their fiscal consequences are well known. The good news is that many policy solutions are available to address this predictable challenge and improve the financial outlook of Social Security.

The Congressional Budget Office has published a report containing over 30 options for improving the long-term stability of the program, including reducing annual cost-of-living adjustments, increasing payroll taxes, lifting the income cap on payroll taxes, reducing initial benefits, and raising the retirement age. The Bipartisan Policy Center also published an extensive report which outlines options for strengthening both Social Security and overall retirement security.

Social Security is an essential program that is relied upon by millions of American seniors. The sooner that we implement reforms, the more gradual they will be, and the easier it will be to secure this critical program.