You are here

10 Key Facts about Student Debt in the United States

While investing in a college education has undeniable, lifelong economic benefits, excessive levels of student debt can impose hefty financial burdens on borrowers — such as restricting how much they can save for retirement, affecting their ability to buy a home, and even delaying life decisions such as starting a family. Those effects are being felt by Americans across the country as young college graduates today are entering the workforce with unprecedented amounts of student debt, and older Americans are still paying off such debt years after graduation.

Below, we explore some key facts on the growth and distribution of student debt in the United States, mostly based on data from the Federal Reserve and the U.S. Department of Education.

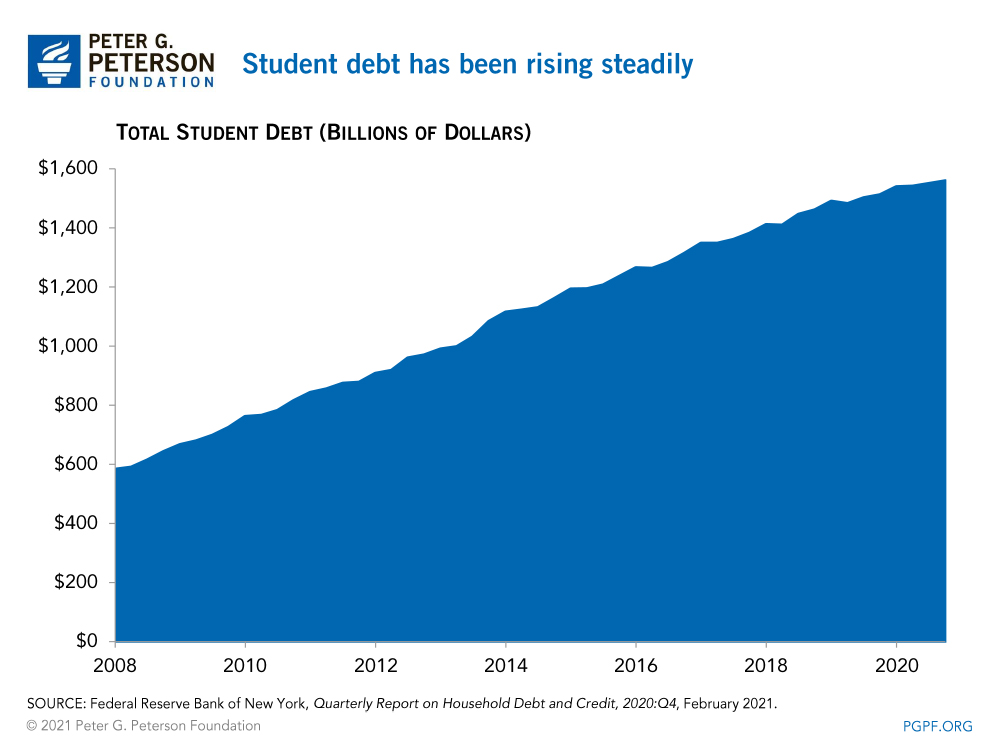

- Student debt has more than doubled since 2008.

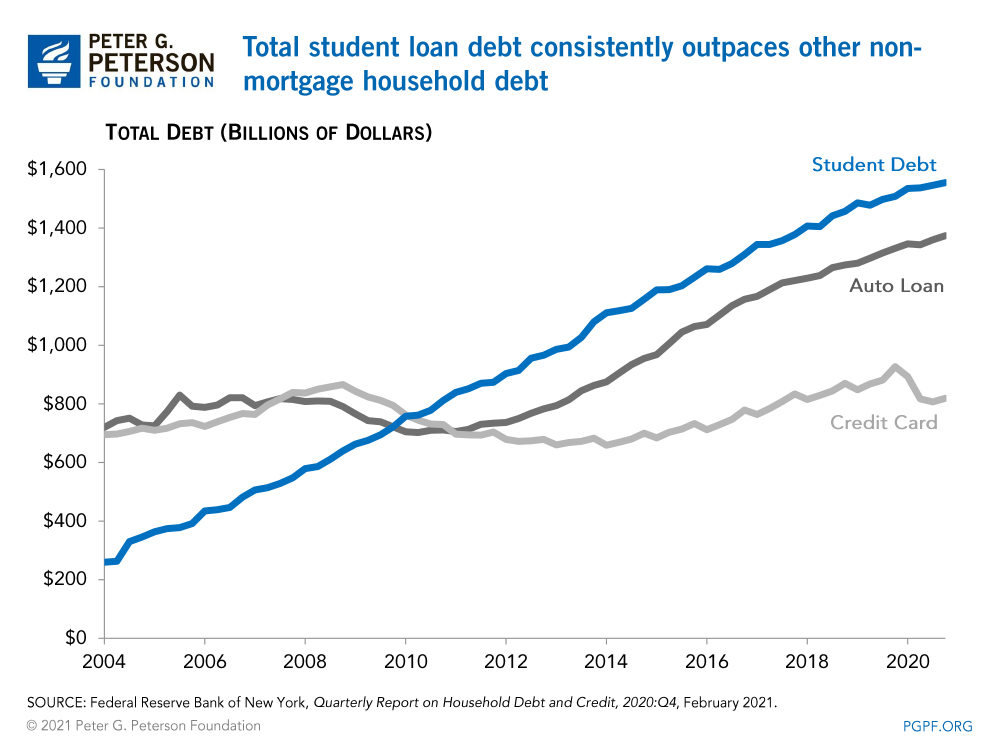

- Student loan debt has been growing faster than other sources of household debt.

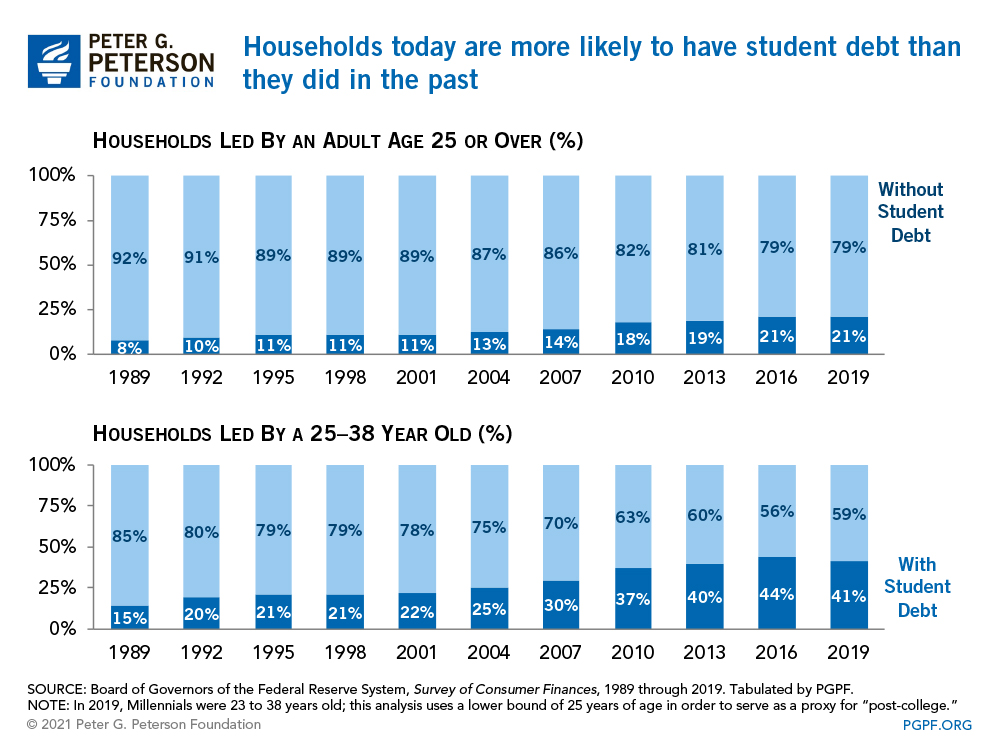

- More adults are burdened with student debt today.

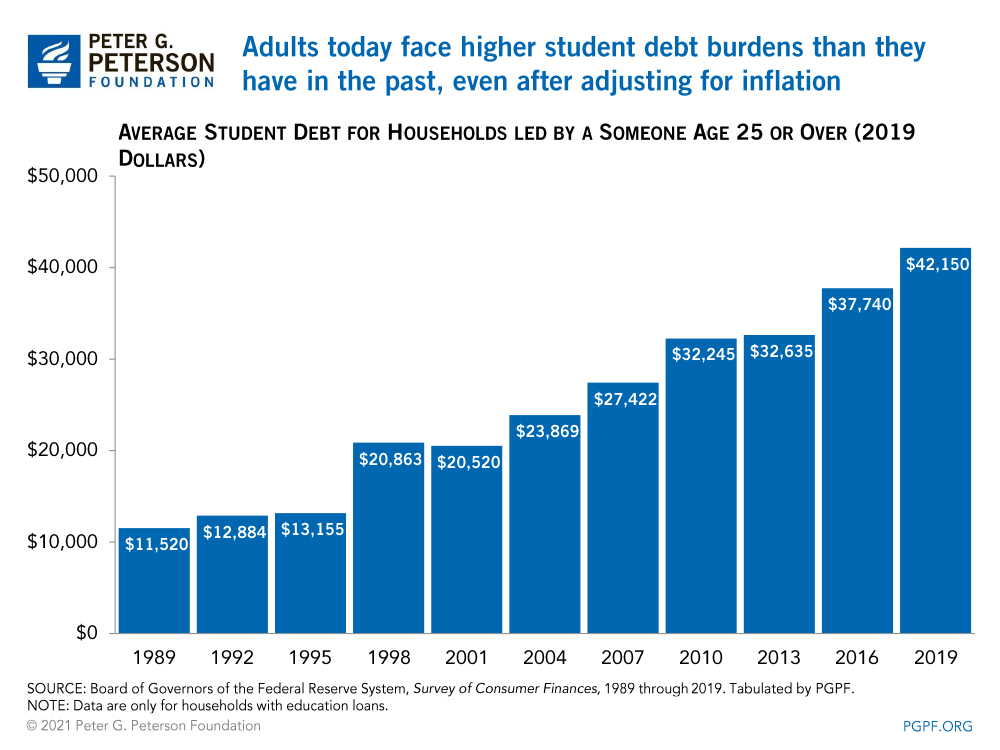

- Adults face a much higher burden of student debt than in the past.

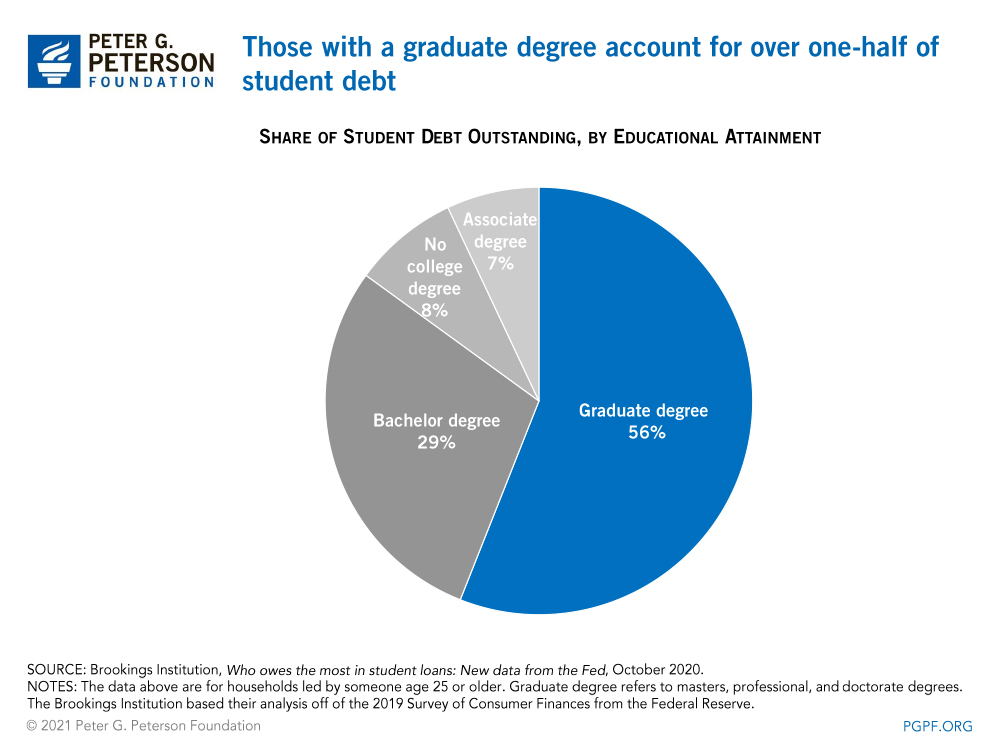

- Graduate school borrowing accounts for most of the student debt outstanding.

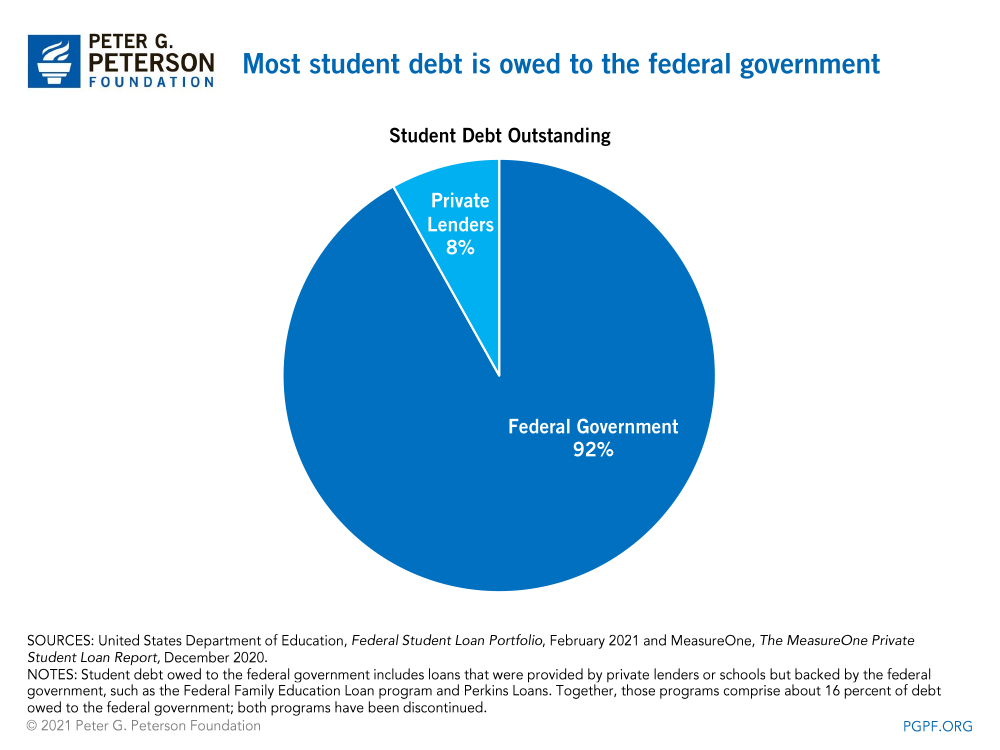

- Most student debt is owed to the federal government.

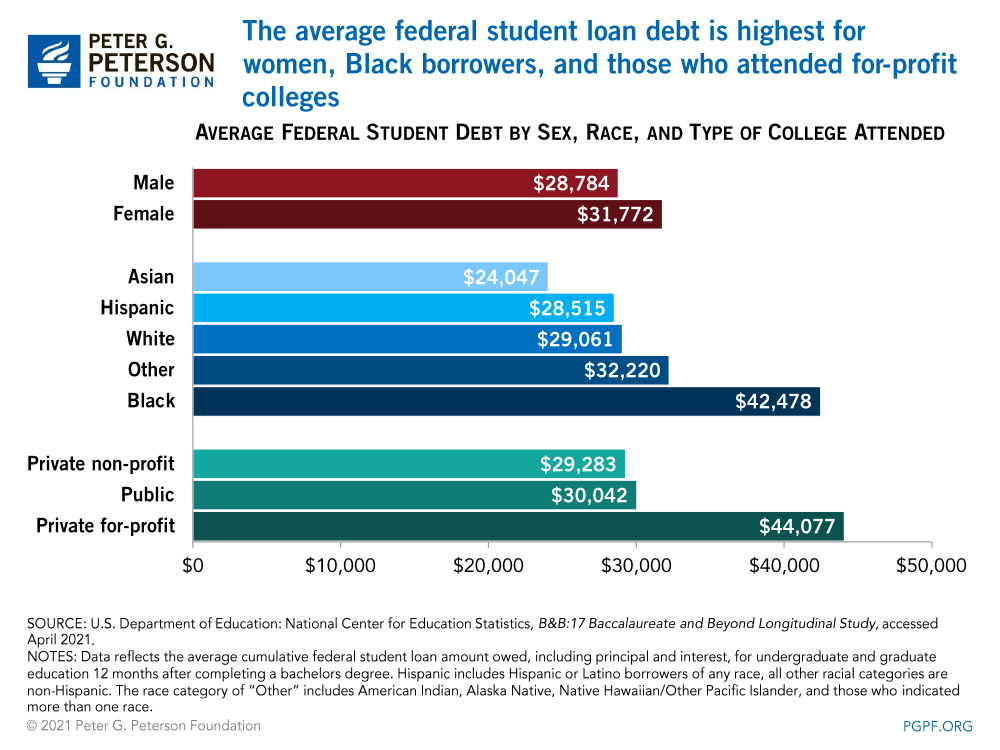

- Women, Black borrowers, and students at for-profit schools owe more federal student debt, on average, than other groups of borrowers.

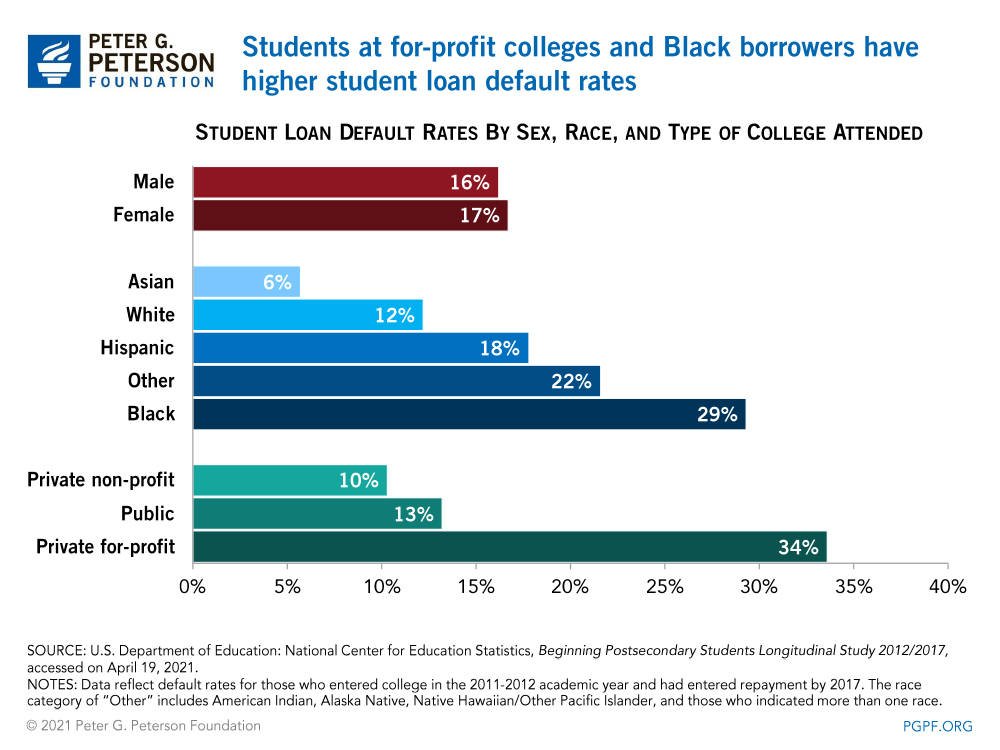

- Students at for-profit schools and Black borrowers have the highest federal student loan default rates

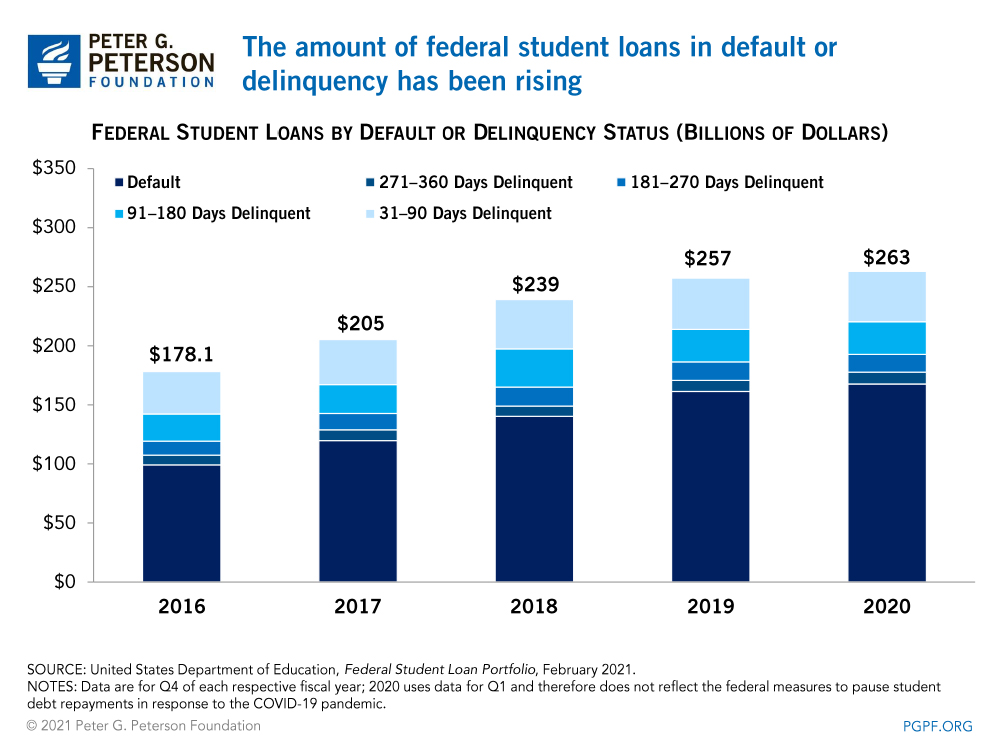

- Overall, the amount of federal student loans in default or delinquency has been rising.

- Student debt may affect the economic outlook for Americans.

The amount of student debt in 2020 totaled nearly $1.6 trillion, more than twice the amount outstanding in 2008 ($600 billion). That growth in debt significantly exceeds the increase in the number of students, which the Department of Education estimates has only risen by 2 percent among undergraduates and by 12 percent at the graduate level.

Since 2004, student loan debt has risen faster than other household debt and has surpassed both auto loan and credit card debt in 2010. Student debt is also the second-largest source of household debt, trailing only mortgage debt.

One major reason for the significant rise in student debt is that more Americans are borrowing to attend college. The percentage of households with student debt has almost tripled, from 8 percent in 1989 to 21 percent in 2019. That trend is true for younger households as well; the prevalence of student debt for those households has climbed from 15 percent in 1989 to 41 percent in 2019.

The average amount of such debt owed per household has increased substantially over the past several years, which has also contributed to the growth in the total amount of student debt outstanding. Among households that took out student loans, the average amount of such debt owed increased nearly four-fold from 1989 to 2019 — even after adjusting for inflation.

The average borrowing levels for graduate students has grown significantly over the past couple of decades. Between the 1995–96 and 2015–16 academic years, the average annual loan for graduate students grew from $10,130 to $18,210, according to the Urban Institute. By comparison, the average annual loan for undergraduate students grew from $3,290 to $5,460 over the same time period. Overall, borrowing for graduate education accounts for 56 percent of student debt currently outstanding.

About 92 percent of all outstanding student debt is owed to the federal government, with private financial institutions lending the remaining 8 percent. That distribution marks a substantial difference from a few decades ago when student loans were provided by private lenders, but subsidized and backed by the federal government.

On average, women owe nearly $3,000, or 10 percent, more student debt than men. Black borrowers owe over $13,000, or nearly 50 percent, more than white borrowers. Factors such as enrollment rates in graduate school programs, type of college attended, and economic outcomes after graduating can affect those debt levels. For instance, those who attended private, for-profit colleges owed about $14,000, or around 50 percent, more than borrowers who attended public or private, nonprofit schools.

Primarily due to higher average debt levels as well as lower earning and employment outcomes, the default rate is highest for borrowers who attended for-profit colleges compared to nonprofit and public schools. In the most recent data available, 34 percent of students who began their education at a for-profit school in the 2011–2012 academic year, and entered repayment of their federal loans by 2017, defaulted on their loans. Partially due to higher enrollment rates at such schools, Black borrowers also have a high default rate, at 29 percent — more than double the 12 percent default rate of white borrowers. Women default on their federal loans at about the same rate as men, 17 percent and 16 percent respectively.

Before the federal government temporarily paused payments on federal student loans because of the COVID-19 pandemic, the number of such loans in default or delinquency status was rising. In the past few years, the amount of such loans increased nearly 50 percent — rising from $178 billion in 2016 to $263 billion in early 2020.

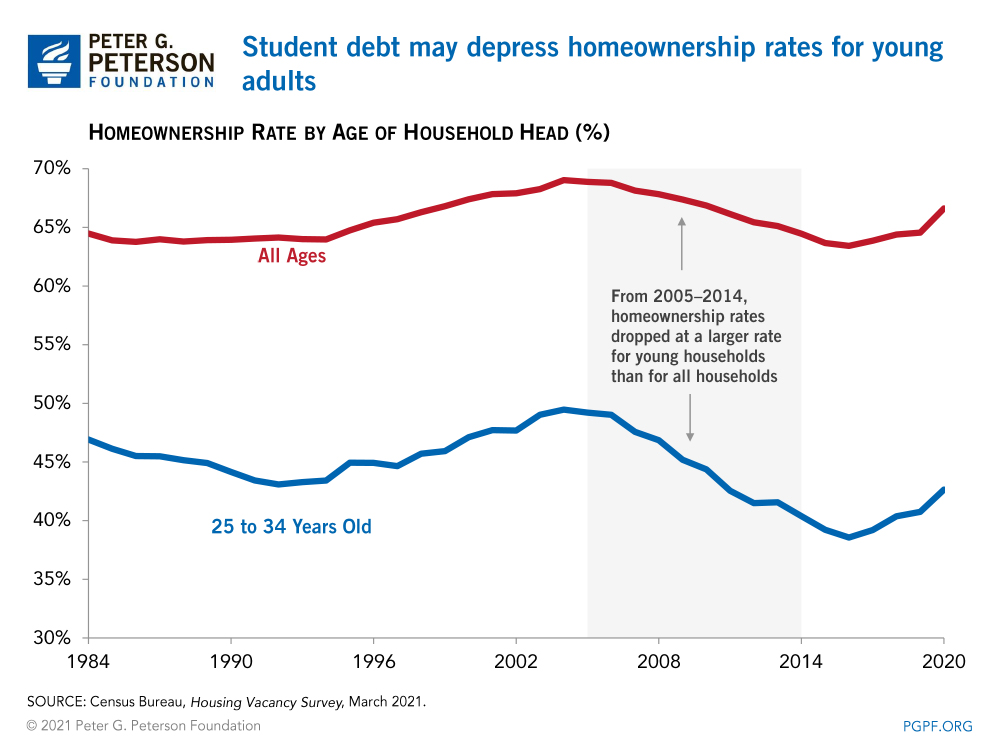

Research by experts at the Federal Reserve indicates that student debt may depress the homeownership rates of households led by young adults. From 2005 to 2014, the homeownership rate for all households dropped by 4 percentage points while the rate for households led by someone age 25–34 dropped by nearly 9 percentage points. Other research has suggested that student debt can affect other aspects of the economy as well — hampering the growth of small businesses, limiting how much Americans can save for retirement, and even delaying marriage and family formation.

Image credit: Photo by Prasit Rodphan/Getty Images/iStockphoto