You are here

How Does the Capital Gains Tax Work Now, and What Are Some Proposed Reforms?

The capital gains tax is a levy on the profit received from the sale of a capital asset. That profit, known as a capital gain, is taxed at a lower marginal rate than ordinary income. While revenues received from taxing capital gains are modest, accounting for 11 percent of individual income tax receipts, changes to the tax could have significant implications for the country’s fiscal and economic health.

Below is a brief look at how the tax on capital gains works, what assets and individuals are most affected by it, and the fiscal implications of some commonly discussed changes.

How Does the Capital Gains Tax Work?

Capital gains are realized when a capital asset is sold for a profit. For example, if shares of corporate stock were purchased for $100,000 and sold 10 years later for $200,000, the $100,000 profit would be considered a capital gain and enjoy a preferential tax rate. Additionally, if a capital asset is sold at a loss, some or all of that loss may offset other gains or be deducted from taxable income. Finally, if the owner of an asset passes away and bequeaths it to someone else, the value for tax purposes will be adjusted to reflect its current value at that time; that readjustment in value is known as the step-up basis.

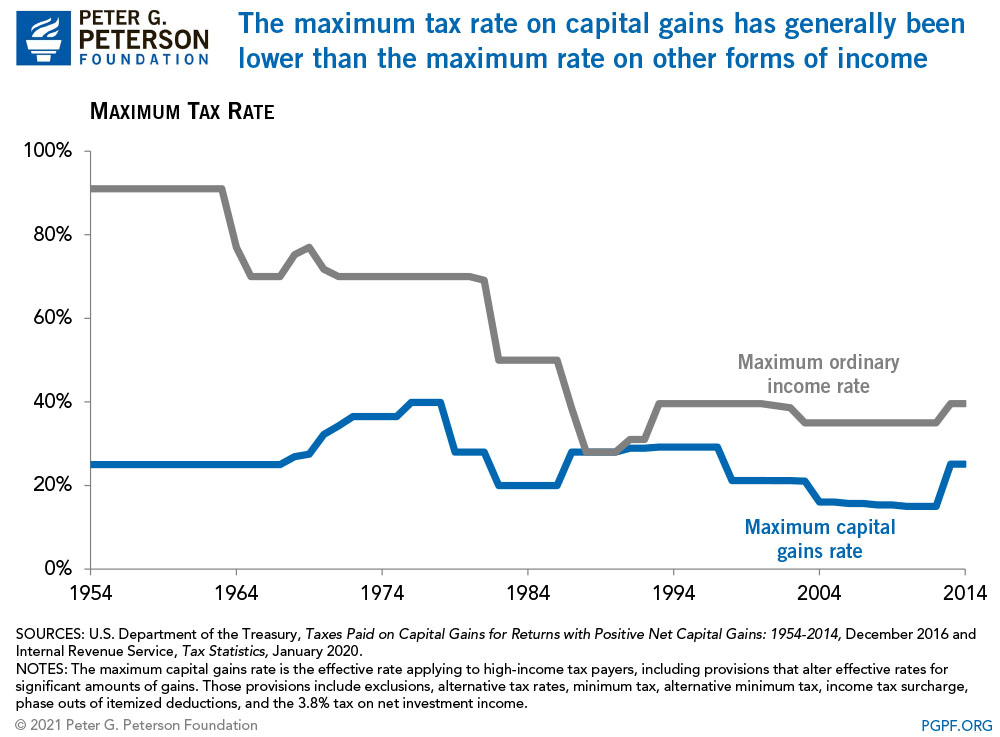

Capital gains on assets that are held for less than one year are known as short-term capital gains and are currently taxed at the same rate as ordinary income for individuals. Capital gains on assets that are held for more than one year are known as long-term capital gains and most are taxed at rates of 0, 15, or 20 percent depending on an individual’s income. Historically, the capital gains tax rate for long-term assets has been lower than the maximum ordinary income tax rate.

What Kinds of Assets are Subject to the Capital Gains Tax?

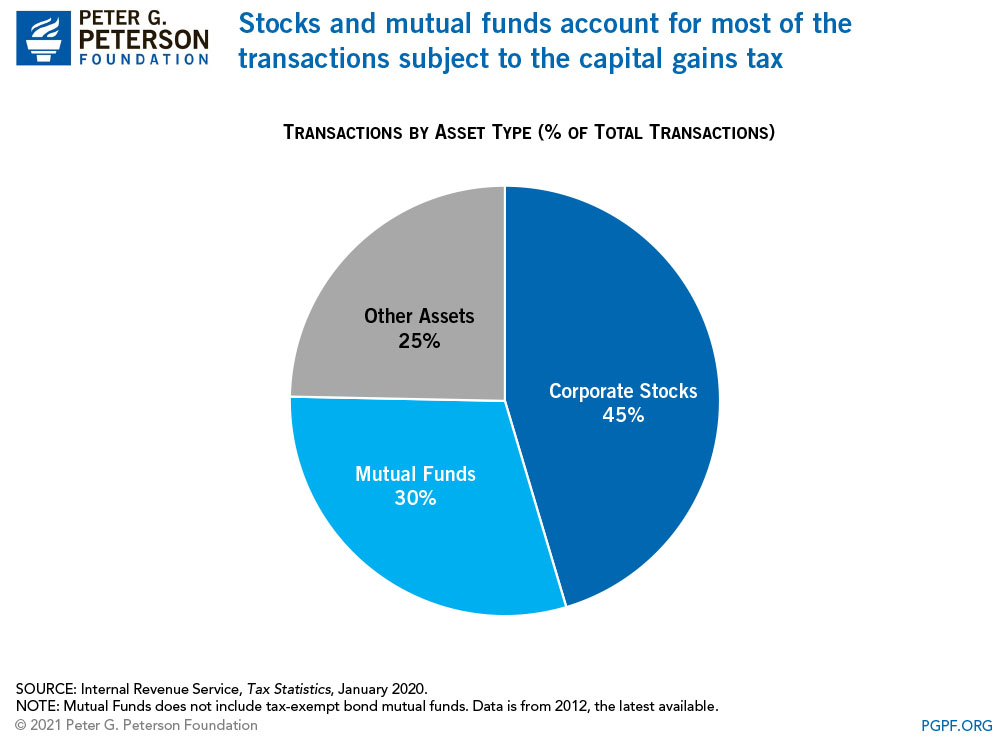

Most of what an individual owns, including securities like stocks and bonds or even “hard” assets such as real estate, can be considered a capital asset. However, most transactions subject to the capital gains tax consist of investments such as stocks and mutual funds. In 2012, the latest year for which data are available, 75 percent of taxable transactions were from stocks and mutual funds.

Who Pays the Capital Gains Tax?

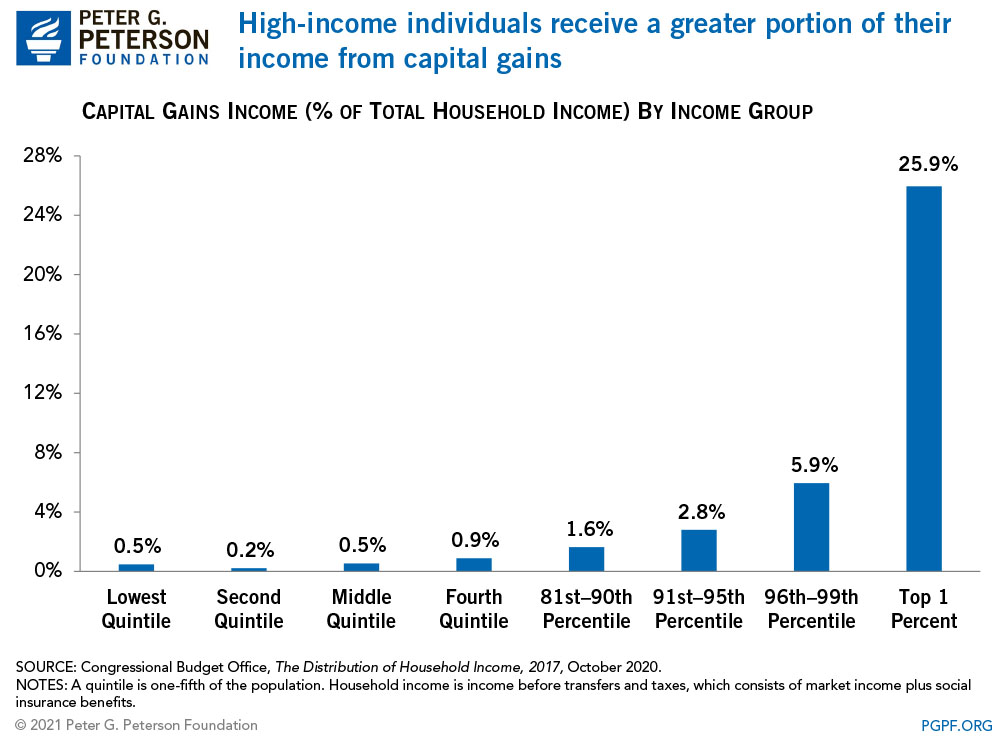

While the capital gains tax affects anyone selling a capital asset, higher-income individuals are typically subject to the tax more so than average Americans. In 2017, individuals in the top 1 percent received about 26 percent of their income from capital gains. That figure compares to less than 1 percent of income for individuals in the bottom 80th percentiles.

How Much Does the Government Receive From Capital Gains Taxes?

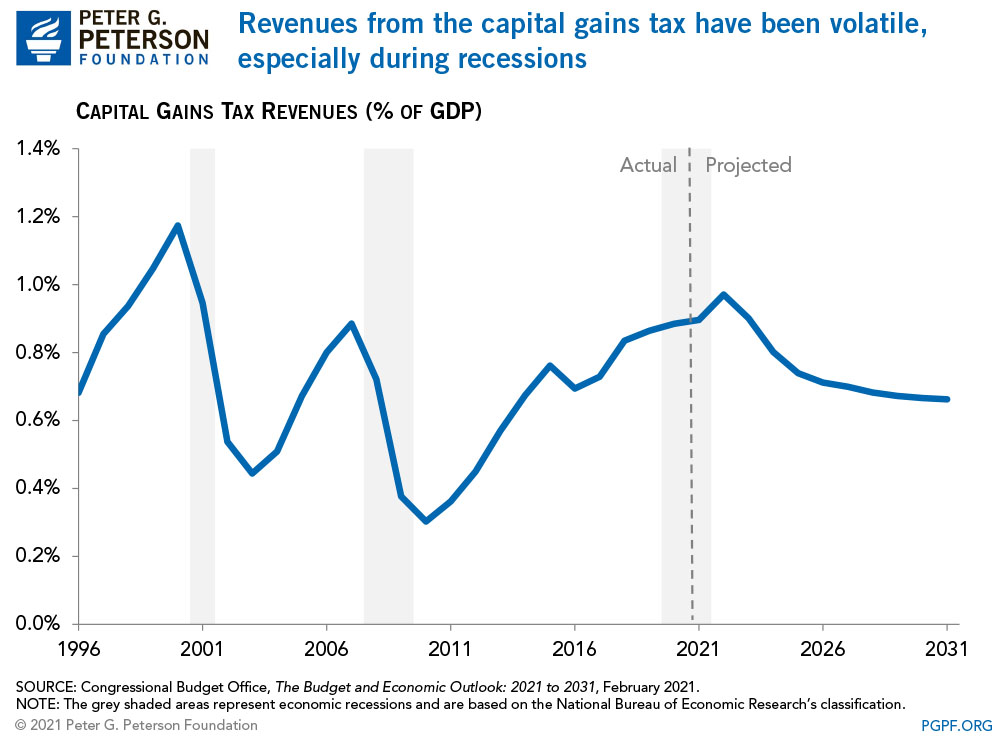

Revenues from the tax on capital gains are categorized as part of individual income tax revenues, but they generally account for a modest portion of such collections. In 2019, the most recent year for which data are not affected by temporary distortions resulting from the pandemic, taxes from capital gains constituted about 11 percent of individual income tax revenues, totaling $183 billion or 0.9 percent of gross domestic product (GDP).

Revenues from the capital gains tax can be volatile, reflecting changes in economic activity — especially during recessions. For example, revenues from capital gains dropped from $100 billion in 2001 to $58 billion in 2002, a 41 percent decrease in just one year. That same pattern occurred during the financial crisis over a decade ago, with capital gains revenues decreasing by 49 percent from 2008 to 2009. However, that trend was not repeated during the current downturn; revenues from capital gains are expected to increase marginally during 2020 and 2021, driven by rapid growth in housing sales — which saw existing home sales increase by 6 percent in 2020 — and the stock market (the S&P 500 rose 16.3 percent in 2020).

Despite the recent growth in capital gains revenues, the Congressional Budget Office anticipates that receipts from the tax will decline to 0.7 percent of GDP, or 7 percent of individual income tax revenues, by 2031.

How Could the Tax Change and How Would It Affect our Fiscal Situation?

Recently, the Biden Administration proposed reforms that would restore the top marginal income tax rate to 39.6 percent, and, for households making over $1 million in a year, apply that rate to long-term capital gains. The plan also calls for the elimination of the step-up basis. In general, proponents of increasing the tax’s burden note that it could raise additional revenues and promote a more equitable tax system that treats different kinds of income more uniformly. On the other hand, advocates for reducing the tax’s impact argue that doing so may increase economic growth and promote entrepreneurship. Below are a number of potential changes — including those proposed by the Biden Administration — that have been discussed in recent years and their fiscal impact:

- Increasing the capital gains tax rate. Such an increase could be applied to one or more of the capital gains tax rates. However, some experts suggest that the higher the tax rates on capital gains, the more likely it is that individuals will wait to sell their capital assets, therefore deferring the tax due. Accounting for such tradeoffs, the Penn Wharton Budget Model estimated that increasing the top rate from 20 percent to 24.2 percent would increase revenues by $66 billion over a 10-year period.

- Removing the ‘step-up’ basis of capital gains at death. Currently, if the owner of a capital asset passes away and bequeaths that asset to someone else, the basis of the asset will be adjusted to reflect the asset’s current value at that time. For example, an asset that was purchased for $100,000, bequeathed and inherited at $180,000, and sold later at $200,000 would have a capital gain of only $20,000. Removing that step-up basis would subject the full $100,000 profit to a capital gains tax. In 2019, the Joint Committee on Taxation estimated that such a policy would increase revenues by $105 billion over a 10-year period.

- Taxing capital gains on an accrual basis. Instead of taxing capital gains when an asset is sold, an accrual system would tax the annual increase in an asset’s value, even if the asset were not sold (also known as a mark-to-market system). While such a system would involve an annual valuation of capital assets and likely require significant resources from the Internal Revenue Service, it would limit the amount of capital gains that are deferred and raise a significant amount of revenues. Tax policy experts at New York University estimated that an accrual system limited to only marketable assets for the top 1 percent of households would raise around $1.7 trillion over 10 years.

- Indexing capital gains to inflation. Currently, capital gains are not adjusted for inflation over the time in which the asset was held. Such an adjustment would decrease the income subject to taxation, thereby reducing the capital gains tax burden. For example, a $10,000 purchase in June 2008 had the same buying power as $11,516 in June 2018; if sold at that date for $20,000, the seller would be subject to a capital gains tax on $8,484 as opposed to the original $10,000 profit. The Tax Policy Center estimated that such a change could decrease federal revenues by $20 billion per year.

Conclusion

The capital gains tax is a relatively small but crucial component of our tax system. Modifying the tax treatment of capital gains is one way that the current administration has proposed to collect more revenues to offset the cost of other proposals. The discussion about our fiscal foundation is an important one; as the country recovers from the pandemic, lawmakers should look at both the revenue and spending sides of the budget and work together to find solutions that chart a more sustainable fiscal path.

Related: Six of the Largest Tax Breaks Explained

Image credit: Photo by Spencer Platt / Getty Images