You are here

Strengthening Medicare: Options to Increase Revenues

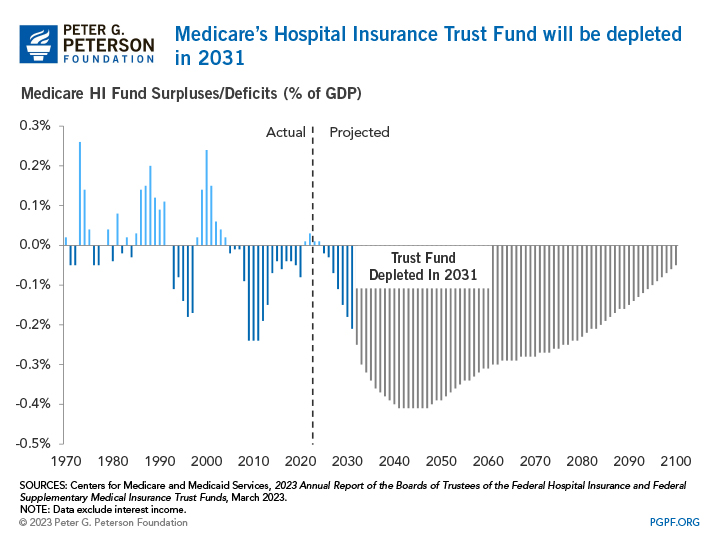

Medicare is an essential federal program that provides health insurance to millions of older Americans. Because of the aging of the population and rapid growth in healthcare costs, enrollment and spending on the program have skyrocketed since its inception almost 60 years ago. One component of Medicare is the Hospital Insurance (HI) program, which covers expenditures for healthcare services related to hospitals, skilled nursing facilities, home health and hospice care. That program is funded by taxes and other inflows to a trust fund, which is at risk of becoming depleted by 2031. Upon depletion, HI payments to providers would be reduced by 11 percent, which could affect services provided to 77 million enrollees at that time.

Many options exist to shore up the solvency of the HI Trust Fund; they can be broadly grouped into reforms that increase the revenues dedicated to the trust fund and ideas that reduce Medicare’s costs. Here we examine modifications that would increase the revenues dedicated to the HI Trust Fund.

How Is the Hospital Insurance Trust Fund Financed?

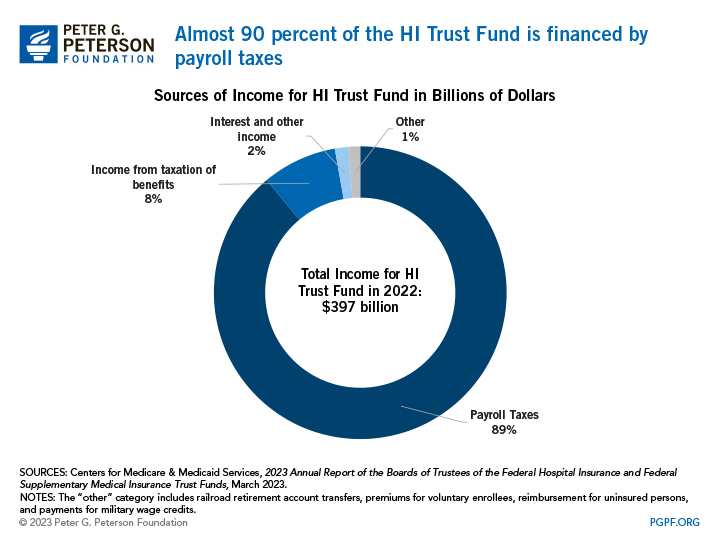

The HI Trust Fund is primarily financed by a 2.9 percent payroll tax, half paid by the employer and the other half by the employee. Additionally, a 0.9 percent tax is applied to individual filers making over $200,000 a year ($250,000 for married households). There is no taxable maximum for the Medicare payroll tax. Income from payroll taxes came to $353 billion in 2022, representing 89 percent of the total income for the trust fund that year. The remaining 11 percent of inflows to the fund comes from taxation of Social Security benefits, premiums for voluntary enrollees, interest on its balance, and a few miscellaneous sources.

Why Is the Trust Fund at Risk?

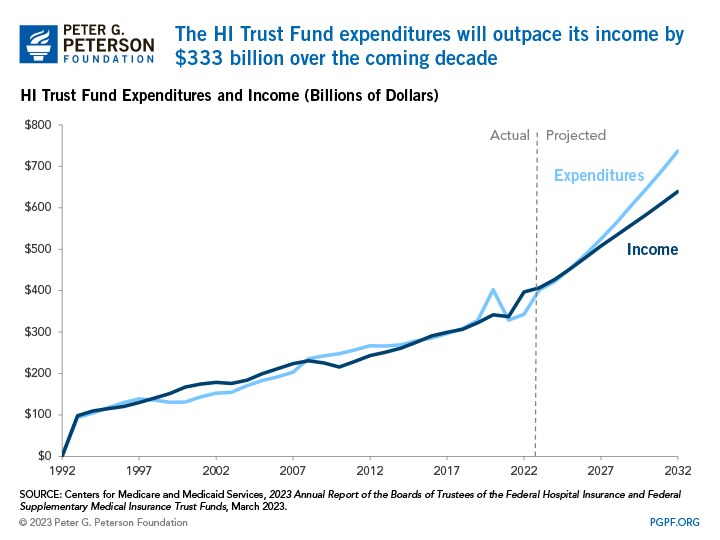

The HI Trust Fund risks depletion because outlays are outpacing revenues. Spending for components of the program, also known as Medicare Part A, have grown quickly. Growth in spending can be linked to demographic trends, increased utilization of services, and rising prices. The aging of the population leads to increases in Medicare enrollment and greater utilization of Part A services. Revenues are not growing fast enough to keep up with those trends, especially because the ratio of workers per beneficiary is declining. In addition, prices for medical care typically grow at a faster rate than inflation, thereby further boosting costs. Such forces combined lead to a projected financing gap of $333 billion over the next decade, according to the Medicare Trustees. If the trust fund becomes depleted, it will only be able to make payments equal to incoming receipts.

What Policy Options Exist to Increase Revenues Dedicated to Medicare?

One side of the financing problem is a shortfall of revenues relative to the cost of the program. Most options to increase revenues relate to the payroll tax, since that is where most funding for the trust fund stems from today. However, other options exist that are less directly tied to Part A of Medicare.

Policy Option 1: Increase the Medicare Payroll Tax Rate

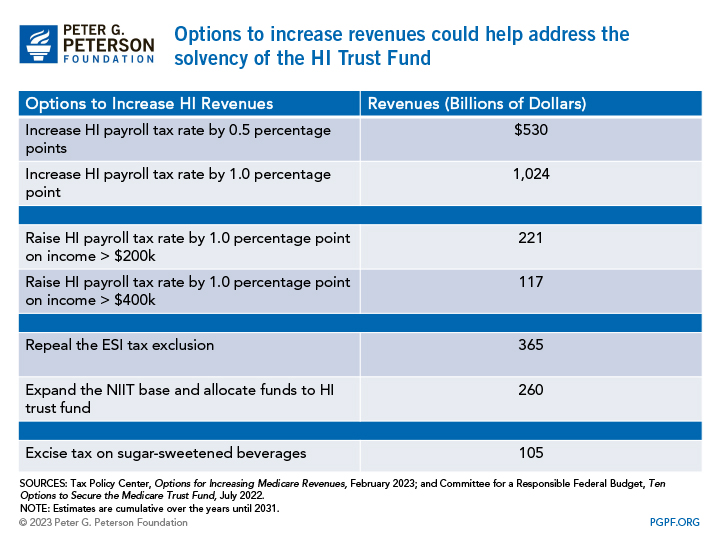

Raising the rate of the payroll tax would bring in more revenues for the program. According to a 2022 analysis from the Committee for a Responsible Federal Budget (CRFB), raising the HI payroll tax rate by 0.5 percentage points in total (0.25 percentage points for both employers and employees) could generate $530 billion over 10 years. Similarly, if the combined employer and employee tax rate were increased by a full percentage point, it would bring in more than $1 trillion over the next 10 years. That amount is more than sufficient to fill the HI’s financing gap over the next decade but not enough to cover the projected long-term growth in HI’s costs.

A variation of the aforementioned proposal would be to increase the combined Medicare tax only for wealthy individuals. Increasing the HI tax by 1 percentage point for a single household earning $400,000 (or $500,000 for couples) and above would raise $117 billion over 10 years. Broadening that increase to those with income more than $200,000 (or $250,000 for couples) would bring in $221 billion.

Proponents of increasing the payroll tax rate believe it would be simple to administer because it would not involve major changes to the tax system. Both employers and employees are accustomed to paying payroll taxes, so an increase in the rate would not make taxes more complicated. Proponents also contend that a marginal increase of just 0.25 or 0.5 percentage points to an employee’s payroll tax is not likely to result in significant additional financial strain for a majority of Americans.

However, others note that increasing the payroll tax could disproportionately affect lower-income households because they typically receive a larger share of their income in the form of wage earnings. Those earnings would be subject to the payroll tax, whereas higher-earning households rely on other forms of income, like capital gains, that are taxed differently. The Congressional Budget Office (CBO) notes that a consequence increasing the tax rate would be that it would incentivize employers to shift compensation to tax-free benefits such as health insurance, which also disproportionately favors those in higher-paying jobs.

Policy Option 2: Expanding the Scope of the Payroll Tax

Broadening the scope of the payroll tax would also help raise revenues for the HI Trust Fund. Two ideas proposed in the President’s Budget over the past two years concern employer-paid premiums for health insurance and the Net Income Investment Tax (NIIT).

Repeal the Exclusion for Employer-Sponsored Health Insurance (ESI)

Under current law, premiums for health insurance paid by employers on behalf of their employees are exempt from income and payroll taxes, even though they are a form of compensation. It is one of the largest tax breaks in the U.S. system. The Tax Policy Center (TPC) finds that repealing the ESI tax break could increase federal revenues by $414 billion over a decade.

A benefit of taxing employer-based premiums is that it would be relatively straightforward because the policy would not be tied to income thresholds or other criteria. Repealing the ESI subsidy would also be indirectly progressive (meaning the tax rate increases as the taxable amount increases) for two reasons. One, it could correct the fact that families at the bottom of the income scale currently receive the smallest subsidy, but pay the highest share of their income on health insurance. And two, higher-income households tend to receive their health insurance through an employer more so than lower-income households, so many lower-income households do not reap the benefits of the ESI tax break. The policy could also reduce total healthcare spending because higher taxes would incentivize employers to offer plans with lower premiums that exclude high-cost providers and services, thereby reducing the usage of high-cost or unnecessary health services.

If the ESI tax exclusion were repealed (either partially or completely), the cost of coverage would likely increase for workers because they would have more responsibility in cost-sharing with their employers and their premium contribution would be taxed. Additionally, employers might offer plans with fewer covered services or narrower networks. CBO estimates that 3.5 million fewer people would have employer-sponsored health insurance by 2032, which could drive people to find coverage elsewhere. Increased enrollment in Medicaid, the Children’s Health Insurance Program, and nongroup market insurance would result in an increase in outlays for those programs, but the net effect would still result in higher revenues for the HI Trust Fund.

Expanding the Net Income Investment Tax

Another way of broadening the tax base would be to expand the base for the Net Income Investment Tax (NIIT) and allocate additional revenues to the HI Trust Fund. The NIIT is currently a 3.8 percent tax imposed on certain investment and business income of high-income taxpayers, but if it were expanded to include certain business owners not subject to Medicare taxes for incomes over $200,000 ($250,000 for married households), it would add $260 billion to the fund over the next 10 years.

A benefit of focusing on the NIIT is that it would close the tax loophole on “pass-through” businesses, which are limited partnerships and S-corporations that are not subject to the corporate income tax. The way the law currently stands, owners of these types of businesses can avoid the tax if they are actively involved in the business, but the reform would treat all high-earners the same regardless of how their receive their income. It is a progressive tax since more than 80 percent of the tax increase would be paid by families in the top one percent of income.

Opponents of this reform option argue that any tax on capital reduces incentives to invest. The capital from investment enhances labor productivity and leads to economic growth. Furthermore, some experts suggest that taxes on capital gains would lead to individuals waiting to sell their capital assets, therefore deferring the taxes they owe.

Policy Option 3: Dedicate Other Sources of Revenues to the Fund

Dedicating revenues from other taxes could also help sustain the HI Trust Fund. One idea is to impose a federal excise tax of 3 cents per 12 ounces on sugar-sweetened beverages. Similar taxes have been implemented in a few states, France, the United Kingdom, Mexico, and Hungary. Revenues from such a tax would add $105 billion to the trust fund over a 10-year period.

A benefit to the sweetened-beverages tax is that it could lead to a healthier population. Multiple studies have shown an association between frequently drinking sugar-sweetened drinks and issues of weight gain, type 2 diabetes, heart disease, kidney disease, and tooth decay. Adding a tax on those drinks could incentivize manufacturers to make beverages with less sugar and drive consumers to purchase healthier options. The tax is also feasible to implement because the federal government already imposes a similar tax on spirits based on alcohol content.

However, the addition of such a tax could disproportionately affect consumers with lower incomes because they consume more sweetened drinks, on average, than those with higher incomes. Furthermore, if soda becomes too expensive, consumers could move to other unhealthy substitutes. One study from Cornell University found that soda taxes prompted many consumers to switch to beer.

Conclusion

In less than 10 years, Medicare’s HI Trust Fund is slated to be exhausted. With 66 million Americans who currently rely on Medicare coverage and a growing number in the future, ensuring the solvency of the fund is crucial to support the insurance program. The sooner reforms are implemented, the easier it will become to secure the financial stability of Medicare. In addition to the options described above to increase revenues into the program, there are a number of available policies that would reduce costs.

Related: Strengthening Medicare: Options to Reduce Costs

Image credit: Spencer Platt/Getty Images